The geostationary satellite has spent six decades getting bigger. The logic was straightforward: a slot 35,786 kilometers above the equator is expensive to reach and valuable to hold, so you fill it with as much spacecraft as the launch vehicle will carry. The result is a fleet of multi-tonne machines that cost hundreds of millions of dollars and take years to build — economics that work fine for an operator serving a continent, and not at all for one that needs to cover a single country, plug a coverage hole, or replace an aging bird whose only remaining job is to keep a legacy service alive.

SWISSto12, a Swiss company based in Renens, near Lausanne, has spent the past several years arguing that the answer is a GEO satellite roughly the size of a washing machine. On July 16, 2026, it announced a $70 million Series C to accelerate production of that satellite — reported in euro terms as a 61 million euro round — on the back of more than $500 million in contracts and $140 million in 2025 revenue.

That last number is the one worth pausing on. In a sector where the standard narrative is "promising technology, distant profitability," SWISSto12 says its contracted backlog will drive positive EBITDA in 2026, and that it has grown at a 110% compound annual rate since 2022 — the year it sold its first HummingSat.

What HummingSat actually is

HummingSat is not a startup skunkworks project that happened to find customers. It is an ESA Partnership Project, developed and validated by SWISSto12 at the head of a supplier consortium drawn from nine ESA member states, and funded through the ARTES line — Advanced Research in Telecommunications Systems — inside ESA's Connectivity and Secure Communications directorate. ESA describes the goal plainly: build a new product line for the commercial geostationary telecommunications market.

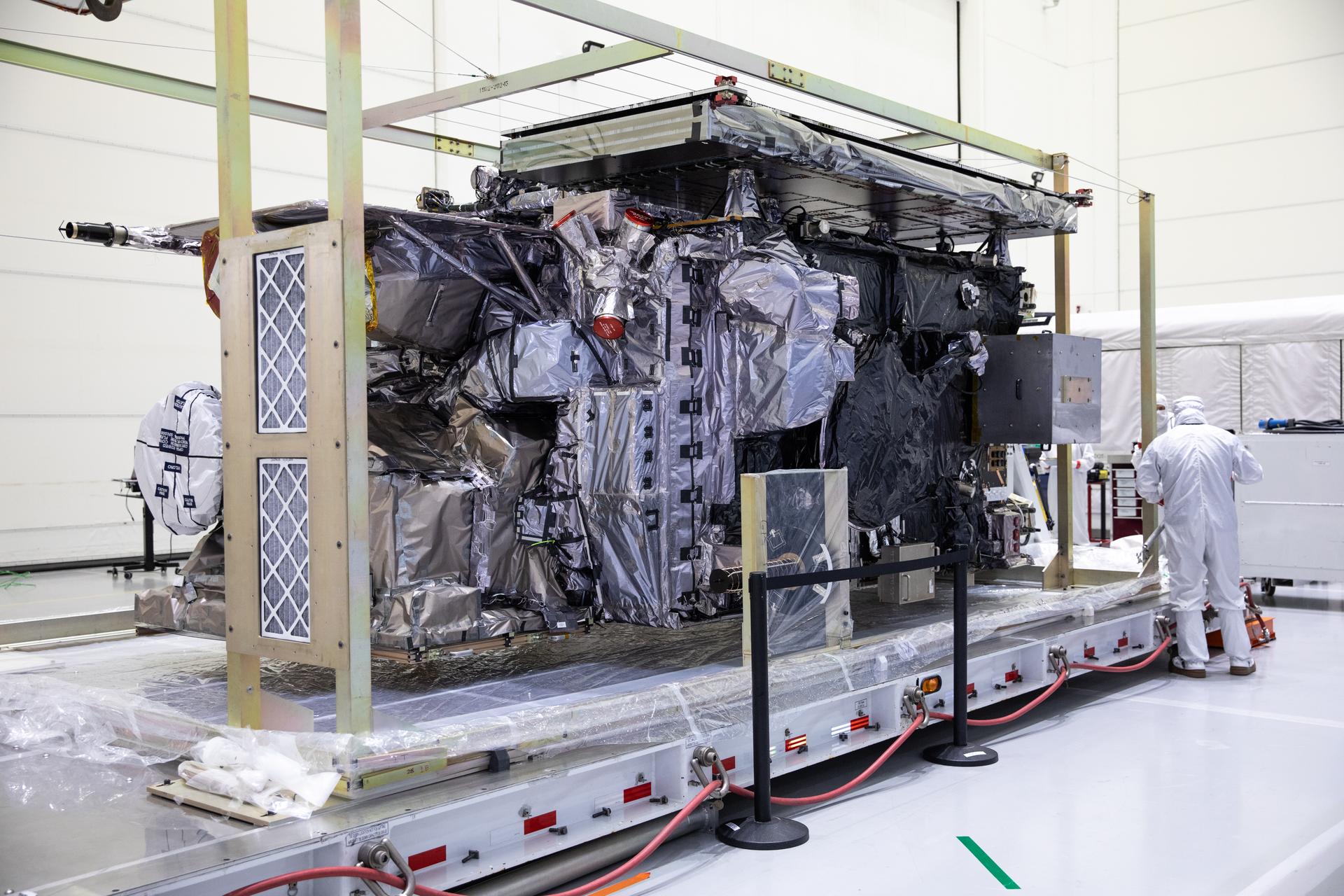

The scale of the departure is easy to state. ESA puts HummingSat at just over one and a half cubic metres in volume — about one-tenth the size of a conventional geostationary satellite. The name is a deliberate joke about the physics: the hummingbird is tiny, agile and fast-moving, yet to the eye it hangs perfectly still.

The technical hook is 3D printing. SWISSto12's business began in radio-frequency components — antennas and subsystems produced additively rather than machined and assembled — using what the company describes as patented 3D-printing technologies to deliver lightweight, compact RF functionality. HummingSat extends that approach to an entire spacecraft, paired with software-defined, reconfigurable payload architectures. The company's pitch is that additive manufacturing reduces the size, cost, and production time of a GEO satellite simultaneously, rather than trading one against the others.

ESA's framing of the payoff is more specific than the usual "smaller and cheaper" boilerplate. Because HummingSats are small and lightweight, they are much more affordable to build and launch, which opens two markets that large GEO platforms structurally cannot serve. The first is bespoke regional or gap-filling service — missions that ESA says would not be financially viable using large satellites. The second is replacement: a competitive option for certain legacy geostationary satellites that have reached the end of their lifetime, where an operator needs continuity but cannot justify another decade-scale capital commitment.

Seven ordered, four named

The order book is where the argument stops being theoretical. Seven HummingSats have been ordered to date, and four customers are on the record. The first to be completed is slated for 2027: Intelsat-45, for SES. Behind it sit four Inmarsat-8 satellites for Viasat in 2028, Neastar-1 for Astrium Mobile in 2028, and SC-A for Space Compass in 2029.

That roster matters more than the raw count. SES and Viasat are established global operators, not speculative buyers — precisely the sort of customers whose existing fleets a small-GEO platform would eventually be replacing, and precisely the sort with every reason to be conservative about an unflown architecture. The 2028 and 2029 dates also show a book that extends well past the first flight, which is the difference between a demonstration and a product line.

No HummingSat is in orbit yet. Everything about the platform's cost and schedule claims remains a claim until a 3D-printed GEO satellite is on station and passing its in-orbit tests, and 2027 is the year the first one is pointed at. The Series C buys production capacity ahead of that proof — which is the normal shape of this bet, but a bet nonetheless.

The sovereignty layer

The July round follows a much larger public commitment. In January 2026, ESA member states put 73 million euros — $84.8 million — behind HummingSat through the ARTES telecoms program. According to SWISSto12, that award was backed at the 2025 ESA Council at Ministerial Level by pledges from Switzerland, Germany, Austria, Sweden, and Norway, plus associate member Canada.

Stack the two together and the private round starts to look like the smaller half of the story. A $70 million Series C sits alongside an $84.8 million public award, which itself sits on a consortium spanning nine member states. The reporting on the round, particularly in European outlets, positions it against rising demand for sovereign European space infrastructure — and the ministerial pledge list reads like a policy decision rather than a procurement one. Six countries do not co-sign a satellite platform because they need one more comsat vendor. They do it because they want the capability to exist on their side of the Atlantic.

This is worth naming clearly, because it cuts both ways. Sovereignty demand is a genuine tailwind: it produces patient capital, anchor customers, and political cover that a purely commercial competitor would have to earn the hard way. It also means some fraction of HummingSat's momentum is downstream of European industrial policy rather than of the platform beating incumbents on price in an open fight. Both things can be true, and the 2027 flight is where they start to get disentangled.

Why It Matters

The small-GEO idea has been floated repeatedly and has mostly foundered on the same rock: geostationary orbit is expensive enough that shrinking the satellite doesn't shrink the mission cost proportionally, so the economics never close. SWISSto12's answer — attack manufacturing cost and lead time through additive production, and target the missions large platforms are structurally bad at rather than trying to beat them head-on — is at least a coherent theory of why this attempt might land where others didn't.

What makes it notable right now is the financial shape. $140 million of 2025 revenue, more than $500 million in contracts, a stated path to positive EBITDA in 2026, and 110% compound annual growth since 2022 describe a company that is being funded to scale a business that already exists, not to discover one. That is an unusual profile in a sector where the modal space company raises against a milestone rather than a P&L.

And it matters for GEO itself. The prevailing story of the past decade has been that geostationary orbit is a declining business, squeezed by low-Earth-orbit constellations. HummingSat's thesis is narrower and more interesting: GEO isn't dying, it's just badly served at the small end. If a washing-machine-sized satellite can profitably fill a regional gap or extend a legacy service, then the constraint was never the orbit. It was the price of the hardware you had to put there.

The 2027 flight will start to settle it.

Sources

- HummingSat — European Space Agency

- Swissto12 raises $70 million to accelerate small GEO satellite production — SpaceNews, July 16, 2026

- SWISSto12 secures 61 million euro Series C amid rising demand for sovereign space infrastructure — EU-Startups

- 73 million euros from ESA member states towards HummingSat — SWISSto12 newsroom